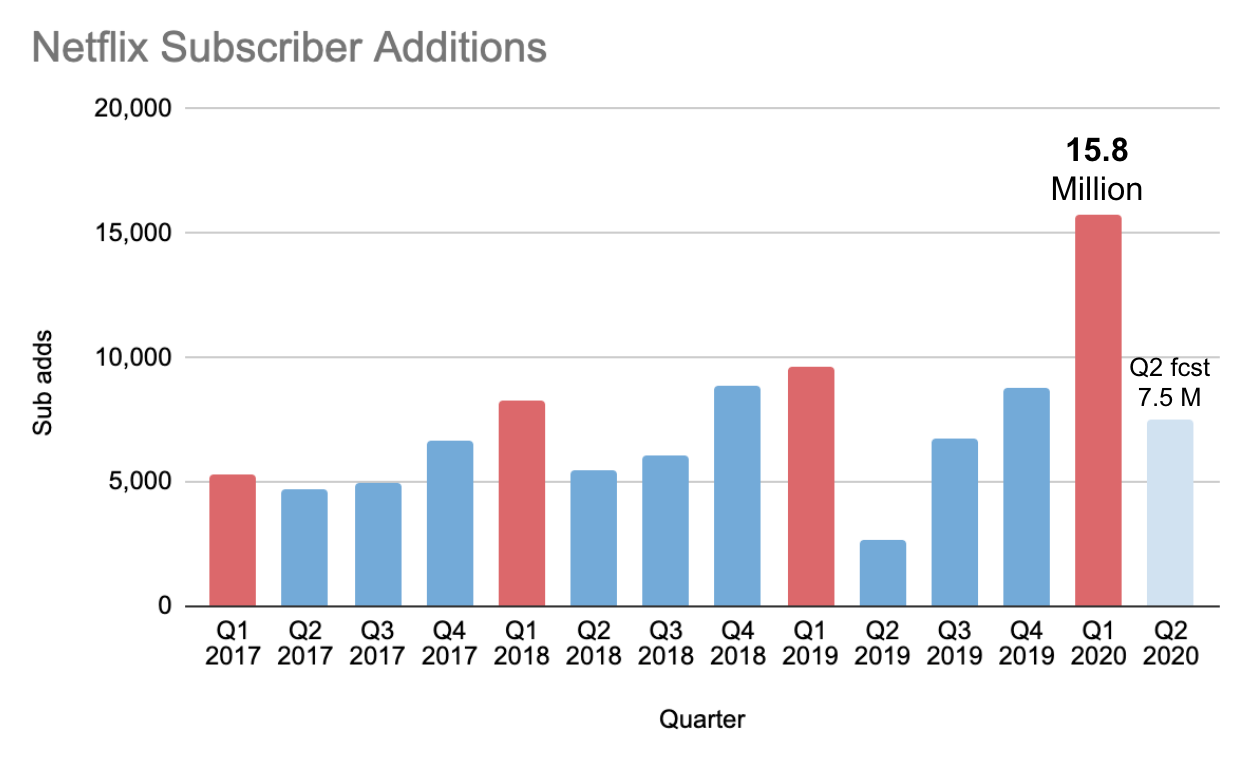

Netflix forecast 7 million new subscribers in the quarter and came in at 16 million. By far their biggest quarter EVER.

They guided to 7.5 million in Q2, which would make that their biggest Q2 EVER.

Corona Crisis is a godsend to Netflix and will accelerate their growth and dominant market positioning.

Obviously we all expected Netflix to exceed guidance this quarter. It was conservative to begin with and people around the world were ordered to stay at home. Some even predicted double digit subscriber additions, but nobody predicted 16 million.

So why didn’t we see a huge rally in the stock price? In fact, it actually went down!

A big (1) is management muted the good news by implying that Q3 and Q4 subscriber numbers would be lower due to a “pull-forward” of demand.

(2) Streaming Wars competition is still a concern and

(3,4,5...) questionable pricing power given competition, foreign currency headwinds hurting revenue and negative cash flow.

Pull-Forward of Demand

This is a phenomenon that Netflix has been talking about for years; usually after they crush guidance, but I cringed when I read the following in the investor letter.

“Some of the lockdown growth will turn out to be pull-forward from the multi-year organic growth trend, resulting in slower growth after the lockdown is lifted country-by-country. Intuitively, the person who didn’t join Netflix during the entire confinement is not likely to join soon after the confinement.”

They may be right, or they may not be. But, for the long-term outlook it doesn’t matter: People all over the world will continue to sign-up and pay for Netflix, because their price-to-value proposition is incredible and recession proof.

Netflix now has over 180 million households paying for its service; so probably 3 - 4x that number of people watching. As more people join the Netflix ecosystem, Netflix will benefit from “network effects”, like Facebook. Meaning if all of your friends are talking about a particular show, you will feel compelled to also watch that show and participate in the social conversation. #TigerKing. #LoveIsBlind.

Well guess what? After the lock down a lot of people are going to be talking about Netflix shows, which will drive continued demand and new sign-ups.

Corona Crisis is accelerating secular trends, including remote working, movie theater death and cutting the cable cord. All three actually bode well for Netflix. Globally consumers were already moving to streaming over cable and because of global stay-at-home orders we are seeing a mass acceleration in the global adoption of Streaming.

AT&T, Verizon and Comcast lost 1.5 million subscribers in Q1, while Netflix picked up 2.3 million in the US and Canada. Some haters even predicted Netflix would actually lose domestic subscribers in 2020.

Streaming Wars Competition

Two areas must be mastered at global scale to compete with Netflix: Technology and Content.

Amazon and Hulu are the biggest incumbent competitors but they’ve been around for many years and have not impeded Netflix growth. Also, worth noting Hulu is only available in the US and Japan. So who are the new entrants?

- Disney+

- Apple TV

- AT&T’s HBO Max (or is Now or Go?...so confusing)

- Comcast’s Peacock

HBO and Peacock are “wait and see”. They’ll probably be ok, but the reality is (1) they are encumbered in profitable legacy businesses (broadband, cellular, cable TV, etc…) and therefore need to navigate corporate bureaucracy and innovators dilemma that will inevitably slow their path (remember Netflix is so focused they split off their DVD division and they have no other operating segments) and (2) they both lack a global technology infrastructure, one that Netflix has been building and optimizing for 10 years.

Apple TV has the global technology infrastructure and they are off to a great start with original content. They also hired Richard Plepler the former head of HBO to a five year contract; a clear signal they are in for the long term and committed to quality. Their biggest issue currently is lack of content; most people would be hard pressed to name two original Apple shows. Nevertheless they will grow over time, but will be many years if ever that they are a substitute for Netflix.

Disney+!

This is the juggernaut that many expect to knock Netflix from their perch. They have global brand recognition and possibly the most valuable content library in the world (particularly when considering their acquisition of Fox). They have passed 50 million subscribers in less than two full quarters. Some question the authenticity of this number as many signed up free thru Verizon in the US and 8 million were automatic via their HotStar business in India. Nevertheless, it’s a meaningful number.

Disney’s global technology infrastructure is weak and will slow global adoption. And while the Disney Corporation owns a lot of great content it is fragmented and licensed to local providers around the world making it difficult to simply “make available” on Disney+; which is why their catalog is thin. In fact, their catalog is largely kid’s content and some blockbuster movies from Marvel and Star Wars. (Pictured is the content they pushed to me via email last week...not exactly compelling). So in short, Disney needs to spend more building their technology and global distribution platform and they need to sacrifice profitability in the short term to build their streaming library and business.

This is where Covid-19 comes in like a wrecking ball. Think about Disney’s big businesses where the profitability comes from:

- Disney theme parks are closed.

- Disney cruise ships are docked.

- Movie theaters are closed.

- Network advertising down significantly.

- ESPN has no sports.

Disney has gone from Streaming Rookie of the Year to a company that literally could be battling to survive the next few months.

Covid-19 won’t kill Disney, but it’s mighty painful.

Other Headwinds Mentioned Above

Cash Flow. Important to acknowledge here is Netflix management (Reed) chooses to be cash flow negative in order to accelerate global expansion and dominant position. This has been a smart move. Finally though, and somewhat a nod to nagging investor concern, Netflix has stated and confirmed that 2019 was peak negative cash flow. Now it’s possible that during 2021 Netflix will flip to positive cash flow, causing a number of value investors to come into the stock and drive up the price. (Netflix actually had positive free cash flow in this quarter, but it's due to shutdown of productions, which by the way should have no effect on 2020 slate).

Pricing Power. This is a valid concern, but as long as Netflix incrementally improves the service they’ll be able to slowly raise prices over years. Think about this: A $1 increase in price globally generates over $2 billion of annual revenue.

Foreign Currency. Can’t do much here. But the negative short-term impact came from US Dollar strengthening during this global crisis. We’ll likely see foreign currencies strengthen when this is behind us.

Conclusion

Back in July 2018 Netflix stock price hit $419. So here we are almost 2 years later and the stock floats around the same level, but with 60 million more subscribers and an even more dominant market position.

My guess is that 2020 will be a record year of subscriber adds and new Netflix stock highs and more great original content!

Thank you Netflix for providing some much needed relief and entertainment in these times!