9 of the top 10 Global Shows in 2020

Stock price at all time high of $590

The Haters have been burned

Now to $700 and beyond

Netflix delivered big in 2020 and Q4 was the cherry on top. Besides beating their 4th quarter paid subscriber forecast by 2.5 million (a 42% beat), they confirmed break-even cash flow expected in 2021 and positive cash flows going forward.

About a year ago when the stock was trading around $350, I wrote what it would take for Netflix to achieve $500 price and move to $700 and beyond. Delivering >30 million subscribers in 2020 and positive cash flows were top on that list.

Full disclosure: I hold Netflix shares and have encouraged my friends and clients to do the same.

So Netflix stock is now trading around $590 - an all-time high - with a market capitalization of $260 billion (Disney is about $315b). I believe undoubtedly that Netflix will continue to grow and move higher over time. Netflix will grow to a $500 billion market cap and its stock price will increase to over $1000; the only question is will this happen in 2-3 years or 5+ years.

First, a little fun look back...

Netflix Haters

My favorite long time hater of Netflix is Michael Pachter of Wedbush Securities; screaming “sell” since 2012. Worried his consistently erroneous predictions damaged the reputation of the firm, his own co-workers asked him to stop covering Netflix.

And then about 1 year ago, Laura Martin of Needham and Co., a graduate of Stanford and Harvard, said Netflix would lose millions of US subscribers in 2020 from the entrance of competing lower priced services.

And of course David Einhorn, renowned manager of multi-billion dollar hedge fund Greenlight Capital said the Netflix narrative was “busted”; too much competition and too much debt.

There have been many other haters of Netflix over the years. How can so many people be so wrong?

The thesis from an analytical and technical standpoint was that Netflix could not withstand sustained competition (i.e. streaming wars) and Netflix was burning too much cash and assuming too much debt. Netflix disproved both those theses in 2020.

Always in play in finance and the world is the psychological bend of certain folks wired to hate. We all know some, rooting against the success of others. Some are short sellers and don’t-pass-line craps players. If you see one, consider exploiting their blind cynicism and negativity for profit.

Now to $700 and beyond

Again, Netflix is going to $700 and then to $1000; the real question is how long will it take? This is important from an investment perspective as you weigh opportunity cost.

Content: At risk of stating obvious, Netflix needs to continue pushing quantity and quality...GLOBALLY. The media here in the US is so focused on the US competition; we hear very little about how the streaming wars are shaking up globally. But Netflix's real growth opportunity is international APAC and EMEA; and this is where they are extending their lead. As a great example, Netflix recently announced they are leasing studio space in South Korea where they have invested over $700 million on content over the last few years.

Subscriber Growth: Again, at risk of stating obvious, Netflix needs to continue to grow subscribers at a steady clip of at least 30 million per year. I hope Netflix presses absolute subscriber growth over average revenue per subscriber (ARPU); the argument being it is more vital to build the global Netflix eco-system, maximize Netflix in global cultural conversations, and then figure out how to extract as much revenue as possible.

Setting audacious goals and targets would be helpful. Netflix is modest compared to how Elon thinks. A goal of 40-50 million subscribers per year would be more appropriate; and stop talking about demand pull-forward already.

China: With a population of 1.4 billion people, Netflix has to continue to knock on their door. Apple and Tesla have had tremendous success in China and so will Netflix. It's rumored that Bob Iger is on Biden’s short list for US Ambassador to China. Bob might have a plan to get Disney+ and streaming overall into China. An announcement into China would translate to an immediate 20%+ bump in valuation.

Sports: I’ve been banging this drum for awhile, but sports creates a new growth opportunity for Netflix and hopefully they will dip their toes in the water. I appreciate Reed’s relentless focus; and it has paid off. But he and the management team are highly capable, and expanding into live sports makes sense now, particularly from the tech side of the house.

Netflix is better at tech than any entertainment company; way better. Netflix has the potential to change the way we watch sports; creating material incremental value viewers will pay for. Disney is moving there now. Imagine what Netflix could do:

- Switch camera vantage points and zooming in/out at viewer discretion.

- Rotating audio feeds among different announcers, coaches and players.

- Grabbing/recording specific plays and sending to your friends.

One’s imagination could run wild here. Consumer Control, a Netflix motto and conspicuously absent from sports.

There are hurdles: sports are expensive and seemingly require advertising to be profitable; the latter not congruent with Netflix’s philosophy and biz model. But, Sports is an area ripe for disruption and who better than Netflix to give it a go.

Conclusion

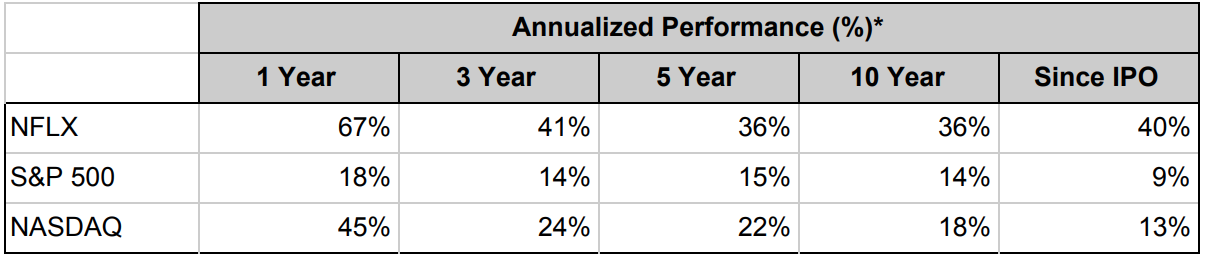

For now let’s just celebrate Netflix’s great execution. Oh and they were kind enough to calculate for us their annual return since IPO: 40%. Reed even made a comment on the call in reference to that number, “if that’s underachieving then we’ll do more of that!”.

Pretty damn good.